The IFRS 15 standard has the merit of replacing, together with the IAS 18 standard, all interpretations. Whether it concerns SIC 31, IFRIC 13, IFRIC 15, or IFRIC 18; IFRS 15 seems to have addressed the specific questions that these interpretations answered. However, the issue of cross obligations has never been raised. In practice, many of us have faced this reality.

By cross performance obligations, we mean a situation in which the seller is obliged to suspend their service and wait for the client to perform theirs before continuing: for example, in the case of a customs broker who, after having taken steps to track the goods from the border to their declaration point and having declared the goods, will wait for the client to pay the customs duties to obtain the remaining documents and facilitate the consumption of the goods.

Such scenarios can also exist in public contracts. For example, the provider will wait for the issuance of an exemption before consuming the materials to meet the next performance obligation, or in the case of events when the client is responsible for paying a rental fee, etc. Therefore, there are cross obligations when the seller must interrupt their service that has already begun and for which they have incurred a cost, waiting for a performance from the client to continue, and this performance is either qualitatively or quantitatively sufficiently material and contains the risk of non-occurrence.

Conditions for recognition under IFRS 15

We all know the conditions for revenue recognition, namely:

- The identification of a sales contract:

- The contract must have commercial substance;

- The contract has been approved by the parties to the contract who have committed to fulfilling their respective obligations;

- The rights of both parties can be identified;

- The payment terms are stated in the contract;

- The collection of revenue must be probable: to assess whether it is probable that it will collect the amount of the consideration, the entity should only consider the customer's ability and intention to pay that amount of consideration when it is due.

- The determination of performance obligations

- The determination of the contract price

- The allocation of a specific price to each performance obligation

- The recognition of revenue whenever a performance obligation is satisfied

In this classic and simple framework, there are complex scenarios, particularly deferred revenue when we are faced with deferred performance obligations or in the case that will be the subject of our article today, that of cross-performance obligations.

Relevance conditions

We will consider three conditions without which our approach loses relevance:

- The dependence of the sales provider

- The fact that the provider has incurred costs upfront

- The existence of the risk of non-occurrence of the customer's performance

The existence of the dependence of the sales provider

We will consider that the provider is dependent on the action to be taken by the client when the latter is not on the same or previous Gantt charts compared to their own. In other words, the next action to be taken by the provider can only be done when the client has fulfilled their service obligation.

If the action to be taken by the client does not prevent the progress of the service, the revenue will then be recognised naturally after verifying the five conditions stated above.

The existence of a cost incurred

The relevance of this reflection also stems from the loss that the provider could incur if the progress of their service were suspended in the absence of the client's service.

At first glance, it should be noted that the standard indicates that there is no contract if one of the parties can unilaterally terminate a contract that has not been fully executed without compensating the other party. If the contract does not contain an explicit, legal, or implicit component that obliges compensation for the service in the event of non-fulfilment of their obligation, the contract will therefore not exist in the sense of IFRS 15 and thus the revenue cannot be recognised.

However, if an implicit or explicit component of the contract or the law and regulations in this area require the client to compensate the provider, at the very least, to the extent of the costs incurred, the revenue may be recognised and thus the cost carried as an asset until the conclusion of the service.

The absence of a constructive obligation to compensate can also be reasonably considered as an indication of the non-existence of a cost to be borne by the sales provider before the client's service.

The existence of the risk of the non-occurrence of the client's service

Without the existence of the risk of non-performance by the client, it would also not be relevant to consider the issue of cross-performance obligations.

We consider that the risk of non-performance by the client is absent or not significant when the resources needed to fulfil their performance obligation are either available or there is no sufficiently material constraint to access these resources.

Recognition conditions – specific aspects

Apart from the conditions stated in the second part, the following specific aspects must be taken into account when recognising revenue in the case of cross-performance obligations.

The existence of the obligation to compensate in the event of non-performance

IFRS 15 informs us that for the purposes of its application, the condition of the existence of the contract will not be satisfied if either party has the unilateral enforceable right to terminate a completely unperformed contract without compensating the other party or parties.

Furthermore, it specifies that a contract is completely unperformed if two conditions are met:

- The entity has not yet provided any of the goods or services promised to the client;

- The entity has not yet received any consideration for the promised goods or services and is not yet entitled to any consideration under the terms of the contract.

We will address the type of performance obligation we are dealing with in the next point. However, we consider that the provider will not have delivered the good or service until the client has fulfilled their performance promise.

We can consider that it will therefore be imperative for the client to have the obligation to compensate the service provider in the event of non-compliance with their service obligation. This constructive or legal obligation will find its source either in business practice considered acceptable, in law, or explicitly in the contract.

The obligation of progressive service

It is important, in our context, to clarify that the standard does not regard the activities that the entity must undertake to execute a contract as service obligations, unless a good or service is provided to the client in the course of these activities. We will therefore refer in our case to acts that provide the client with an asset if the service must be interrupted.

Furthermore, a good or service promised to a client is distinct as soon as the two conditions below are met:

- The client can benefit from the good or service taken in isolation or by combining it with other readily available resources (that is to say, the good or service can exist separately);

- The entity's promise to provide the good or service to the client can be identified separately from other promises contained in the contract (that is to say, the good or service is distinct within the contract).

Let us recall that we have adopted the condition of the risk of the non-occurrence of the client's service. We have also clarified that this risk did not exist when the resource necessary for its execution is available or can be readily available.

On the other hand, it is reasonable to consider that the service is fully performed only after the client's performance and therefore cannot be reasonably identified distinctly in the contract. We can thus conclude that it is a progressive performance obligation.

Indeed, under IFRS 15, the performance is progressive under the conditions that:

- The client simultaneously receives and consumes the benefits provided by the entity's performance as it occurs;

- The entity's performance creates or enhances an asset (for example, work in progress) over which the client gains control as it is created or enhanced;

- The entity's performance does not create an asset that the entity could use otherwise, and the entity has an enforceable right to payment for the performance completed up to the date considered.

Now, we can consider that if the client's performance is a hindrance to the successful completion of the sales performance, then at this stage the client already possesses an economic benefit on which only their performance and the subsequent sales performance remain. It is therefore justifiable to identify a progressive performance. The right to consideration having already been mentioned, the next question that is important to answer is the assessment of this progression.

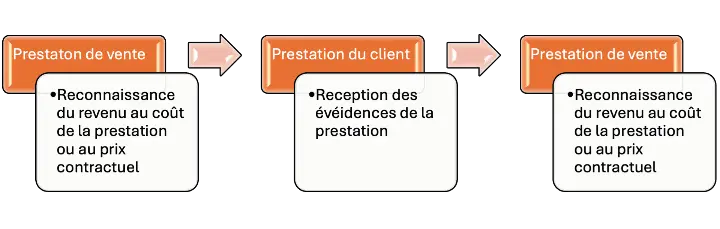

The progressive recognition of revenue

The standard requires progressive recognition for each performance obligation fulfilled progressively. This recognition will be made using the input or output method based on the degree of completion. The entity then recognises revenue using the progress method either by outputs or by inputs.

In our case under study, it seems wise to recognise revenue by the inputs. We consider that the amount of compensation will be at most the cost already incurred by the service provider.

Thus, revenue could be recognised according to this graphical scheme:

The consideration of the financing component

In order to properly assess revenue, IFRS 15 draws attention to the existence or absence of the financing component.

Indeed, it notes that when an entity determines the transaction price, it must adjust the amount of promised consideration to account for the effects of the time value of money if the payment schedule agreed upon by the parties to the contract (explicitly or implicitly) provides the customer or the entity with a significant financing benefit related to the provision of goods or services to the customer.

Conclusion

The conditions that make our reflection relevant are:

- The dependence of the provider on the action to be taken by the customer;

- The fact that the provider has incurred costs upfront;

- The existence of the risk of the customer's non-performance.

If these are met, we believe that the following specific conditions should be taken into account:

- The existence of the enforceable obligation in the customer's performance and the obligation for compensation in the event of non-performance

- The identified performance obligation will be considered as progressive

- The progressive recognition of revenue will be done using the input method

- The assessment of the presence of the financing component